Choosing Your Online Business Model

Starting an online business requires a deliberate evaluation of how value will be created, delivered, and monetized. The selection of a business model determines operational requirements, cost structure, revenue potential, and long-term scalability. It influences daily workflows as well as strategic planning. A clear understanding of the primary online business models helps entrepreneurs align their skills, resources, and objectives with a practical approach.

E-commerce involves selling physical goods through digital storefronts. This model can be executed through self-hosted websites, online marketplaces, or a combination of both. Operators must manage sourcing, supplier relationships, inventory control, packaging, fulfillment, and returns. Some businesses hold inventory in warehouses, while others rely on dropshipping arrangements where suppliers ship products directly to customers. Each approach carries trade-offs. Holding inventory offers control over quality and shipping times but requires capital and storage costs. Dropshipping reduces upfront investment but can limit control over product availability and margins.

E-commerce businesses must also address logistics, including shipping carriers, delivery times, and customer expectations regarding tracking and returns. Pricing strategies typically account for product cost, shipping, packaging, marketing, and transaction fees. Profit margins may vary significantly depending on the niche and level of competition. The model rewards efficiency in supply chain management and strong brand positioning.

Service-based models focus on selling expertise or labor rather than physical goods. Services delivered online include marketing consulting, bookkeeping, graphic design, software development, tutoring, coaching, and legal or financial advisory work. Compared to product-based models, service businesses often require less upfront capital but rely heavily on the expertise and availability of the founder or team. Revenue is frequently tied to billable hours, project fees, or retainer agreements.

One advantage of service-based businesses is simplicity in operations. There is no inventory to manage, and fulfillment often involves digital communication tools. However, scalability may be more limited unless the business transitions into an agency model, hires staff, or develops standardized service packages. Reputation, referrals, and demonstrated competence are central to growth in this model.

Digital products include downloadable or cloud-based goods such as e-books, online courses, templates, software, stock photography, and membership content. After initial development, digital products can often be sold repeatedly with minimal incremental production costs. This creates the potential for relatively high profit margins compared to physical goods. Distribution is typically automated through e-commerce platforms or membership systems.

The primary investment in digital products is time and expertise during the creation phase. Market research is critical to ensure demand. Developers must also consider intellectual property protection, platform hosting costs, and technical support. Although margins can be substantial, competition in digital markets may be significant, requiring strong differentiation and marketing strategy.

Affiliate marketing involves promoting other companies’ products or services in exchange for a commission. Affiliates may use blogs, video platforms, email newsletters, or social media channels to drive traffic to partner offers. Commissions may be based on sales, leads, or clicks. This model does not require product creation or inventory management, making it accessible to individuals with strong content creation or audience-building skills.

Success in affiliate marketing depends on trust, transparency, and audience relevance. Income can fluctuate based on platform algorithms, commission structures, and market demand. Affiliates must also comply with advertising disclosure regulations and platform rules. While the barrier to entry is low, consistent income generally requires a structured content strategy and sustained audience engagement.

Subscription-based businesses generate recurring revenue by offering ongoing access to products or services for a periodic fee. Examples include software-as-a-service (SaaS) platforms, subscription boxes, professional memberships, and content communities. Predictable recurring revenue allows for improved financial forecasting and long-term planning.

This model requires continuous value delivery to minimize cancellation rates. Subscription retention depends on consistent quality, customer satisfaction, and ongoing communication. Metrics such as churn rate, lifetime customer value, and cost of acquisition are central to maintaining profitability. Subscription businesses often benefit from strong onboarding systems and customer support processes.

Each of these models presents different capital requirements, operational complexity, and scaling pathways. Selection should consider available skills, tolerance for risk, time commitment, and long-term goals. Some entrepreneurs combine multiple models, such as selling digital products alongside consulting services or integrating affiliate marketing into content-driven websites.

Legal Requirements and Structure

Once a business model has been selected, attention must shift to legal structure and compliance. Online businesses in the United States operate within federal, state, and sometimes local regulatory frameworks. Understanding and fulfilling these requirements reduces legal risk and improves credibility.

Choosing a business structure is one of the earliest legal decisions. A sole proprietorship is the simplest form, allowing one individual to operate without forming a separate legal entity. While easy to establish, this structure does not separate personal and business liabilities. Partnerships involve two or more individuals sharing ownership, profits, and responsibilities according to an agreement.

A limited liability company (LLC) combines aspects of sole proprietorships and corporations by separating personal assets from business liabilities while maintaining relatively flexible taxation. Corporations, including S corporations and C corporations, offer a more formal structure with shareholders, directors, and officers. Corporations may provide advantages for raising capital but involve stricter reporting requirements and formal governance procedures.

Selecting the appropriate structure influences taxation, liability exposure, administrative requirements, and potential investor relationships. Consultation with legal and tax professionals can clarify the most suitable arrangement based on projected revenue and operational complexity.

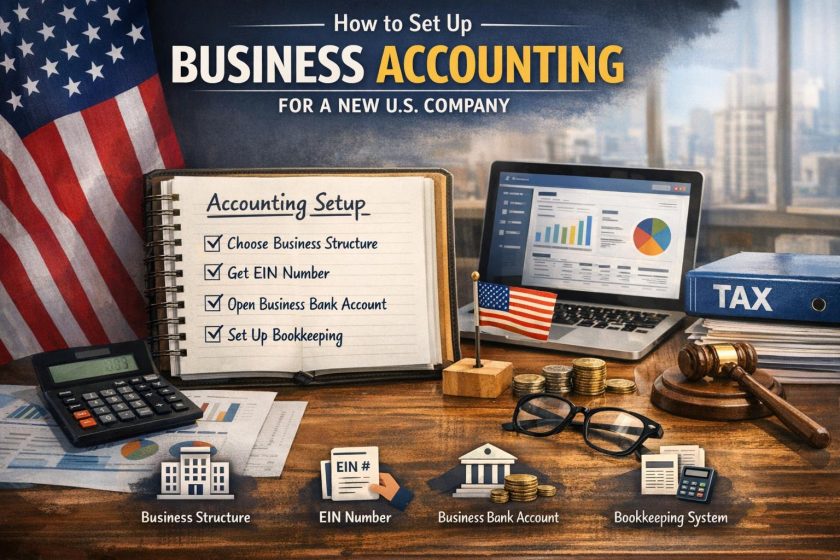

After determining the structure, the business must be registered with appropriate authorities. This typically involves registering with the state in which the business operates. Many businesses must obtain an Employer Identification Number (EIN) from the Internal Revenue Service, even if they do not plan to hire employees immediately. An EIN is necessary for tax reporting, opening business bank accounts, and processing payroll if employees are later added.

Depending on location and industry, some businesses require licenses or permits. While many purely digital service providers may not require specialized permits, regulated industries such as health, finance, or education may face specific licensing requirements. E-commerce businesses selling certain goods may also need sales tax permits or resale certificates. Requirements vary by state and municipality.

Tax obligations for online businesses include federal income tax and potentially state income tax. Additionally, e-commerce businesses may be required to collect and remit sales tax in states where they have established economic nexus, which can be triggered by reaching certain sales thresholds. Understanding multistate tax responsibilities is particularly important for businesses selling nationwide. Keeping detailed financial records and separating personal and business finances simplifies compliance and reporting.

Online businesses must also consider data privacy regulations, consumer protection laws, and advertising standards. Privacy policies, terms of service, and refund policies should be clearly articulated on websites. If customer data is collected, steps must be taken to ensure secure storage and responsible usage.

Setting up the Business Operations

Operational systems convert a chosen model into daily activity. A well-structured operational foundation supports consistency, efficiency, and performance measurement.

Developing a business plan provides structured guidance. Although online entrepreneurship can begin informally, a written plan clarifies objectives and assumptions. Typical components include market research, competitive analysis, customer segmentation, pricing strategy, marketing approach, and projected expenses. Financial forecasts should estimate startup costs, operating costs, revenue, and break-even points. Even a simplified plan enables more disciplined decision-making.

The website functions as a central operational asset. A professional domain name strengthens brand identity and enhances credibility. Web hosting services must provide reliability, security, and sufficient bandwidth for anticipated traffic. Website design should prioritize usability, accessibility, and mobile responsiveness. Clear navigation and concise content promote positive user experiences and reduce abandonment.

Search engine visibility depends on technical optimization, including page structure, fast loading speeds, and accurate metadata. Security features such as SSL certificates protect customer data and build trust. For e-commerce operations, product descriptions, images, and checkout systems must function seamlessly. For service providers, contact forms and scheduling systems should operate efficiently.

Payment processing systems must support secure and compliant transactions. Options include traditional credit card processors, digital wallets, and third-party platforms. Selection depends on transaction fees, integration compatibility, and supported currencies. Transparent pricing and straightforward checkout procedures contribute to higher conversion rates.

Customer interactions require organized handling through effective customer service systems. Even small businesses benefit from structured processes for responding to inquiries, managing refunds, and resolving disputes. Email support, chat services, and automated response systems enhance communication. Customer relationship management software can store contact information, purchase history, and communication logs, improving continuity and personalization.

Additional operational considerations include accounting systems, inventory management software for product-based businesses, and project management tools for service providers. Organized recordkeeping contributes to tax compliance, budgeting accuracy, and performance evaluation.

Marketing and Growth

With operational systems established, growth depends on systematic marketing and performance analysis. Digital channels allow for measurable and targeted outreach, but effective execution requires planning.

Search engine optimization (SEO) enhances visibility in search engine results. This process includes identifying relevant search terms, producing structured content, and improving website architecture. Technical optimization, such as improving load speed and mobile compatibility, contributes to ranking improvements. Content development that addresses specific customer questions or problems helps attract organic traffic over time. SEO is often a long-term strategy requiring consistent updates.

Social media marketing provides opportunities to reach targeted audiences and engage in two-way communication. Different platforms serve distinct user demographics and content formats. Professional services may benefit from platforms that emphasize networking and thought leadership, while visual product brands may prioritize image-focused platforms. Consistent posting schedules, audience interaction, and performance analysis contribute to steady growth.

Email marketing remains a reliable channel for direct communication. Building an email list through sign-up forms, lead magnets, or gated content allows businesses to share updates, promotional offers, and educational materials. Segmented email campaigns can improve open rates and conversion by tailoring messages to specific audience interests or behaviors. Data analysis of open rates, click-through rates, and conversions informs optimization efforts.

Paid advertising, including search engine ads and social media ads, can accelerate traffic generation. Advertising budgets should be monitored carefully to ensure cost-effective acquisition. Calculating customer acquisition cost relative to lifetime value aids in determining sustainable spending levels.

Continuous measurement is essential. Analytics tools track metrics such as traffic sources, time spent on pages, bounce rates, and conversion rates. These data points reveal which marketing channels perform effectively and which require adjustment. Testing variations in headlines, calls to action, landing page layouts, and pricing structures can incrementally improve results.

Growth strategies may also include partnerships, collaborations, and referral programs. Strategic alliances with complementary businesses can introduce products or services to new audiences. Referral incentives encourage satisfied customers to recommend the business to others, leveraging existing relationships for expansion.

As the business grows, operational scalability becomes increasingly important. Automation tools can handle repetitive tasks such as email sequences, invoicing, and onboarding processes. Delegation to contractors or employees may become necessary to sustain service quality and customer support standards. Documented procedures ensure consistent output and facilitate team expansion.

Maintaining stability requires ongoing financial monitoring. Reviewing profit margins, expense ratios, and cash flow patterns supports informed decision-making. Reinvesting profits into marketing, product development, or infrastructure often supports sustained growth.

Online businesses operate within dynamic digital environments. Consumer preferences, technology platforms, and regulatory conditions evolve over time. Regular review of strategy allows adaptation to changing conditions while maintaining core objectives.

By systematically selecting a business model, complying with legal requirements, implementing structured operations, and applying data-driven marketing strategies, entrepreneurs can establish a foundation for sustainable online activity in the United States. Careful planning combined with disciplined execution enables online ventures to expand methodically within competitive digital markets.